The $4,000 House: When American Workers Could Buy Homes Like We Buy Cars Today

In 1952, my grandfather walked into a Levittown sales office on Long Island with $400 in his pocket — money he'd saved from his job at the Brooklyn Navy Yard. He walked out with the keys to a brand-new three-bedroom house. The total price: $7,990. His annual salary: $3,200.

Photo: Brooklyn Navy Yard, via www.brooklynnavyyard.org

Photo: Brooklyn Navy Yard, via www.brooklynnavyyard.org

Do the math. That house cost him exactly 2.5 times his yearly income. Today, using that same ratio, a median American household earning $70,000 should be able to buy a home for $175,000. The actual median home price? Try $400,000.

Something broke in the American equation, and it broke so gradually that most of us didn't notice until it was too late.

When Houses Were Just Big Appliances

In the decades after World War II, buying a house wasn't an investment strategy or a wealth-building scheme. It was just something you did when you got married and needed more space. Houses were consumer goods, like cars or refrigerators, except they lasted longer.

The numbers tell the story. In 1950, the median home price in America was $7,400. The median family income was $3,300. A teacher, a postal worker, or a factory employee could reasonably expect to save for a down payment and own a home within three to five years of steady work.

Compare that to today. A teacher in most American cities would need to save every penny of their salary for five years just to afford a 20% down payment on a median-priced home. And that's before they pay for food, rent, or anything else.

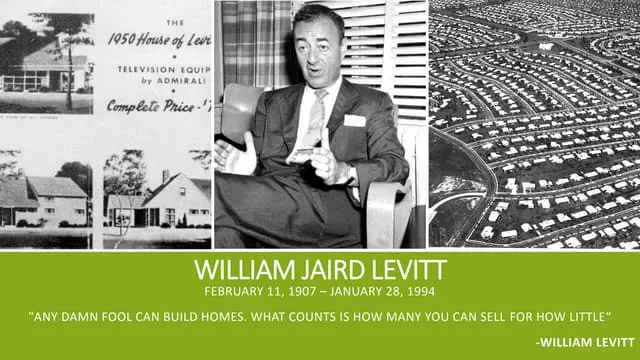

The Levittown Promise

Levittown wasn't just a suburb — it was a promise made real. Developer William Levitt figured out how to mass-produce houses the way Henry Ford had mass-produced cars. Assembly-line construction, standardized materials, and economies of scale brought the price of homeownership within reach of regular working families.

Photo: William Levitt, via cdn.slidesharecdn.com

Photo: William Levitt, via cdn.slidesharecdn.com

These weren't mansions. The original Levittown houses were 750 square feet, smaller than most modern apartments. But they had yards, modern appliances, and something priceless: affordability. A veteran could buy one with no money down using a GI Bill loan. The monthly payment? About $58, roughly what many families were paying for rent.

The formula was simple: build efficiently, sell cheaply, and let ordinary Americans live the dream. For thirty years, it worked.

When the Math Changed

The transformation didn't happen overnight. Through the 1970s, homes remained relatively affordable. A house might cost three or four times a family's annual income — expensive, but manageable with a 30-year mortgage.

Then something shifted. By the 1980s, home prices began rising faster than incomes. By the 2000s, they were rising faster than anything else in the American economy. Today, in many markets, homes cost eight, ten, or even twelve times the median local income.

What changed? Everything.

First, homes stopped being consumer goods and became investment vehicles. Wall Street discovered real estate, and suddenly houses weren't just places to live — they were assets to flip, bundle, and trade. When investors compete with families for the same properties, families lose.

Second, construction costs exploded. Environmental regulations, zoning restrictions, and building codes — many necessary and beneficial — added layers of expense that didn't exist in the Levittown era. Today's homes are bigger, more complex, and far more expensive to build.

Third, land became scarce in desirable areas. The endless suburban sprawl that made Levittown possible ran into geographic and political limits. When you can't build out, you have to build up or pay more for what's left.

The New Math of Homeownership

Today's housing market operates on completely different mathematics than the one that built the American middle class. In 1950, a typical family spent about 14% of their income on housing. Today, financial experts recommend spending no more than 30% — and millions of Americans spend 40% or more.

The old rule was simple: save for a few years, buy a house, pay it off over 30 years, own it free and clear by retirement. The new reality is more complex: save for a decade, compete with investors and foreign buyers, stretch to afford monthly payments that consume half your income, and hope home values keep rising fast enough to build equity.

We've replaced a system that created homeowners with one that creates mortgage holders. The difference matters more than most people realize.

What We Lost When Houses Became Investments

The transformation of housing from necessity to commodity changed more than just prices. It changed the entire social fabric of American communities.

When houses were affordable, people bought them to live in for decades. Neighborhoods were stable. Kids grew up with the same classmates. Local businesses could count on steady customers. Community institutions — churches, schools, civic organizations — could build long-term relationships.

When houses became investments, mobility became the goal. People bought starter homes to trade up to better homes to trade up again. Neighborhoods became way stations rather than destinations. Community became harder to build when everyone was planning their next move.

The Road Back

Some cities and states are trying to recreate the conditions that made homeownership accessible in the postwar era. They're streamlining permitting, allowing denser construction, and experimenting with new forms of affordable housing.

But the fundamental tension remains: as long as homes are both places to live and investment vehicles, the needs of residents and investors will conflict. Making housing affordable for families means making it less profitable for speculators.

The generation that could buy houses for three times their annual income is mostly gone now. They leave behind a country where homeownership — once the foundation of middle-class stability — has become a luxury good.

Whether we can rebuild that foundation, or whether we'll adapt to a world where most Americans remain permanent renters, will define the next chapter of the American story.